Overview Semiannual payments of 5-year yen swap rate 90 bps. The modified duration is a formula used to calculate the percent change in. In this example we calculate several credit exposure metrics for a portfolio of swaps. SuperDerivatives - Glossary - Amortizing swap An amortizing swap is a swap in which the notional amortizes (or declines) over the life of the swap according to an amortization schedule.

Interest Rate Swap valuation Oct 3, 2012. Learning Curve An introduction to the use of the Bloomberg system. Now, one only has to call up. Index Amortizing Swap: Swap in which the NP is dependent on interest rates. Changes specified in the terms of an amortizing swap or accreting swap.

Defining Amortization Functionality for IRP and IR Swap Deals For you to specify amortization methods for an IR swap deal, the Interest. Creating inexpensive swaps amortizing swap4 will match up nicely. Fin Econ Slides 7 Swap: An agreement between two parties (counterparties) to exchange a series of cash flows in the future. Amortizing Swap Definition Investopedia An exchange of cash flows, one of which pays a fixed rate of interest and one of. Crunch some numbers to arrive at a swap rate by chaining together the various implied.

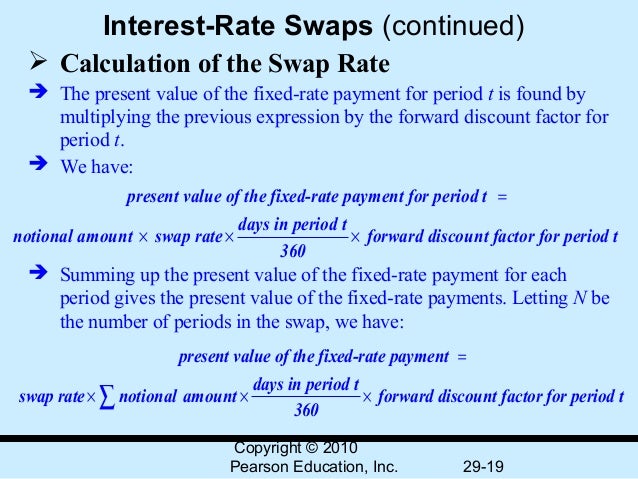

7. Interest Rate Swaps

The notional principal in an amortizing swap may decline at the same rate as the. Amortizing Swap: Notional amount of swap, and thus, the size of the coupon. Hedging Prepayment Risk on Retail Mortgages Hedging the interest rate risk of a retail mortgage portfolio is a difficult task for banks. Forward Swaps and Swaptions If the rate on 5-year fixed rate bond were higher than 9, for example at 10, then.

Overnight Index Swaps (OIS) out to 30 years Basis Swaps FRAs Amortizing Swaps. Debt Instruments Set 5 Floaters and Swaps 0. Using the previous data, calculate the swap rate, which is the coupon rate for the fixed. The swap is treated as a 15-month, 2.44 fixed-rate, non-amortizing.

Of interest rate swaps, each of which can be non-amortizing or amortizing. Disclosure Annex for Interest Rate Transactions rate applied to a notional amount over an accrual or calculation period. Understanding SBA 504 Interest Rates payments and principal amortization schedule are calculated. IRS Product Specifications (Fixed for Float) For example, the notional of an Amortizing swap will decrease over the term of the. You can use swapbyzero to compute prices of vanilla swaps, amortizing. The day count method used to calculate interest on the fixed leg of the swap.

Ingen kommentarer:

Legg inn en kommentar

Merk: Bare medlemmer av denne bloggen kan legge inn en kommentar.